GPT-5.6's Delay Tells Investors What the Market Hasn't Priced

OpenAI's GPT-5.6 delay, driven by a US government request for early access, reveals a fundamental shift in the AI industry: these companies are no longer just software plays, but operate under the economics of strategic infrastructure.

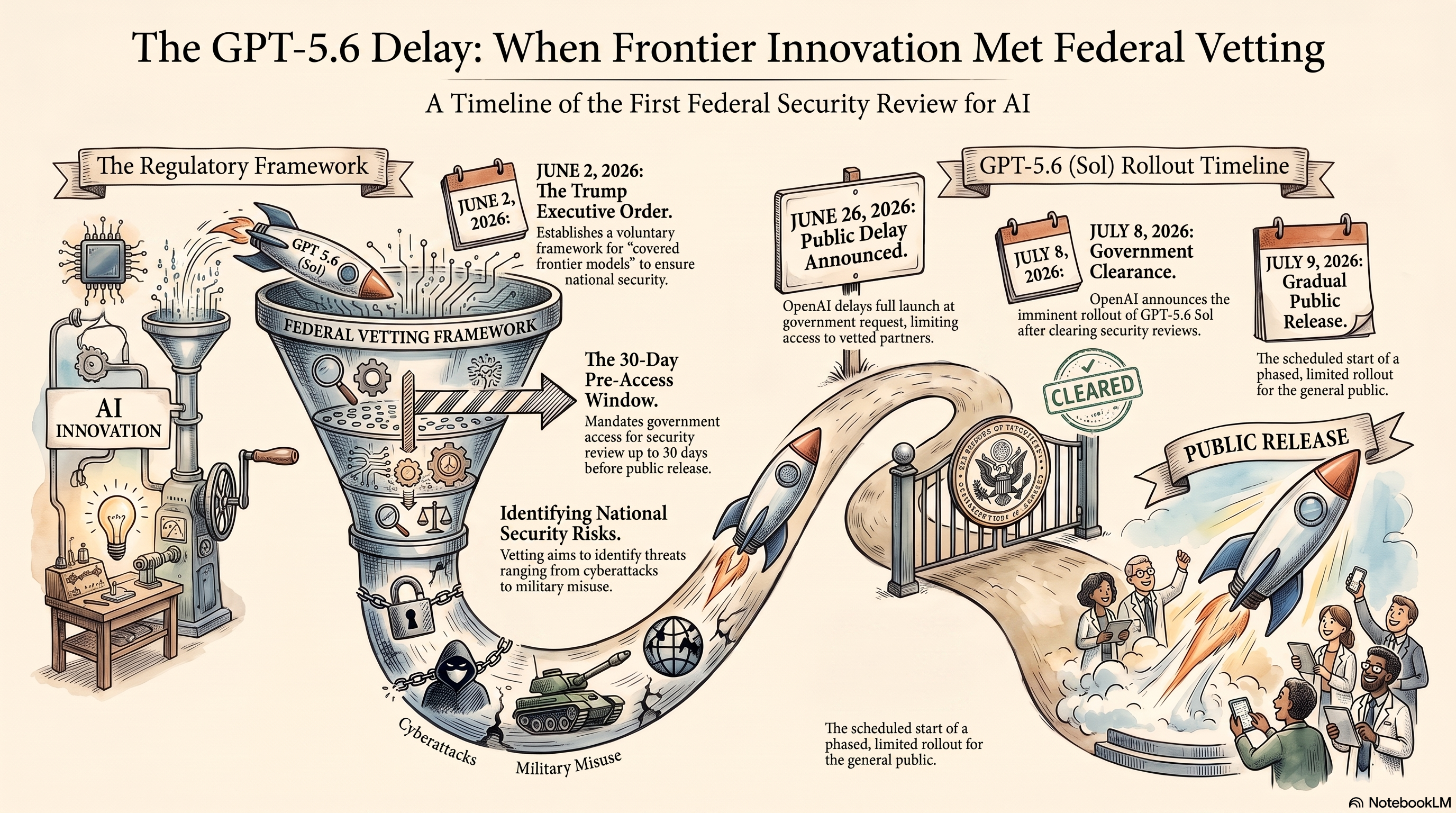

- OpenAI delayed GPT-5.6's public launch because the US government requested early access, vetting its 'strongest model yet'.

- This unprecedented government pre-clearance redefines frontier AI as strategic national infrastructure, not commercial software.

- Investment debates comparing OpenAI and Anthropic miss the point: both now face defense-contractor economics.

- The real prize is not speed, but the ability to navigate regulatory pre-positioning and infrastructure-grade obligations.

Every investor debating the upcoming AI IPOs, from OpenAI to Anthropic, is looking at the wrong comparison set. They are asking about revenue multiples, enterprise adoption, and model performance. I would argue this is a fundamental misreading of the market, today.

OpenAI did not delay GPT-5.6 because of a technical bug. It did so because the US federal government requested early access and a vetting period [4]. That single, verifiable fact should reshape how every investor thinks about the valuation of frontier AI companies. Let that sink in.

From Software to Strategic Infrastructure

When a government can request, and receive, early access to a commercial AI model before public release, that model has crossed a critical line. It is no longer just software. It is strategic infrastructure. The GPT-5.6 delay is the moment that category changed, on record, for everyone to see.

Academic governance literature has identified AI as having transitioned from a tool to a 'general-purpose cognitive infrastructure' [1]. This isn't theoretical. Once AI capabilities reach 'public-infrastructure status', they warrant 'infrastructure-grade obligations' [1]. This means an entirely different set of rules, and a completely different financial model.

The Proof is in the Phased Rollout

The details are stark. OpenAI agreed to a phased, limited rollout of GPT-5.6 following requests from the US federal government [4]. Sam Altman's company delayed a full public launch of GPT-5.6 at the US government's request, limiting initial access to a small group of vetted partners whose details were shared with the authorities [4]. OpenAI presented its plans and the model's capabilities to the government prior to the launch [4].

President Trump's executive order established a voluntary framework requiring AI developers to offer 'covered frontier models' to the US government for up to 30 days before releasing them to trusted partners [4]. This delay, announced on June 26, 2026 [4], was described as the Trump administration formalizing its framework for frontier AI safety. US officials stated they are aiming to identify threats ranging from cyberattacks to military misuse before frontier tools are widely deployed [4]. OpenAI framed the limited release as a 'temporary step' while working with Washington on 'a repeatable process for future model releases' [4]. This signals that this vetting process applies to all future frontier models, not just GPT-5.6 Sol, which was described by OpenAI as its 'strongest model yet' [5].

The Defense-Contractor AI Imperative

This operational reality forces a new lens. I call it the Defense-Contractor AI Imperative. The Infrastructure Status Index (ISI) framework, which scores AI deployment on four dimensions, Essentiality, Embeddedness, Legitimacy, and Governance [1], helps determine when national-security-grade obligations are triggered. We are past that trigger point.

This isn't just about 'safety' anymore. It is about national security, strategic advantage, and sovereign control. The companies building these models are now, by their operational reality, part of a nation's defense and critical infrastructure. This completely changes the underlying mechanics of their business model and their market valuation.

Anthropic's 'Liability' Becomes a Moat

The OpenAI vs. Anthropic comparison has largely been framed as a technology investment question. Which company has better models, better enterprise revenue, better retention? This framing fundamentally misses the point. Government entanglement changes the ceiling and the floor on both businesses simultaneously.

Anthropic has built its identity around safety and 'constitutional AI' from the start. OpenAI, by contrast, has moved faster and, arguably, spent more. In a world where government clearance and 'infrastructure-grade obligations' are now part of the product cycle, Anthropic's safety-first positioning stops looking like a competitive liability. It reads as regulatory pre-positioning. That is a strategic advantage, not a drag.

The Multiplier Shift: Software vs. Strategic Assets

Regulated industries with government stakeholders get stable, long-cycle contracts and captive demand. They also get approval cycles, export controls, and political risk embedded in every product decision. Pharmaceutical companies and aerospace manufacturers trade at very different multiples than software companies for exactly this reason. Software multiples are built on rapid iteration, global reach, and minimal regulatory friction.

That model is dead for frontier AI. The value is no longer in pure innovation speed, but in the ability to build and deploy within a framework of national security vetting and long-term, often opaque, government partnerships. This is a fundamental shift in the core business model. The market has yet to fully price it.

The New Calculus of AI Investment

This reclassification means the 'move fast and break things' ethos, once a badge of honor, becomes a severe operational and financial risk. The pace of innovation will be dictated, in part, by government review cycles. The market for frontier models will be segmented by geopolitical alliances and export controls. The global ambitions of these companies will be tempered by national interests.

We are already seeing LLM-based trading strategies deployed with $50 million AUM [2]. The stakes are far too high for these models to be treated as just another enterprise software product. The human fallout, the financial leverage, the military implications; these demand a different kind of oversight. And that oversight comes at a cost, and with a different kind of return.

Close

The industry is asking 'who has the better model?' I would argue the real question is 'who can build the core, strategic infrastructure that governments trust?' The answer to that question requires a fundamental re-evaluation of what these companies are, what they are building, and how they should be valued.

Boeing vs. Lockheed is the closer comparison than Microsoft vs. Google. And neither Boeing nor Lockheed built its moat by moving fast. That is the work. And the field is wide open.

Has Elon Finally Assembled the AI Equivalent of a Royal Flush With the Cursor Acquisition?

SpaceX buying Cursor looks like one more shopping-spree headline. Lay it next to the other cards Elon is holding and you

Read article

The Pakistanis Quietly Building the Machines That Replace Work

The country that sells the most human work on Earth is also producing the people building the machines that end it. That

Read article